E[aX+b]=aE[X]+b

Note how the Expected Value is shifted by amount b

E[E[Y∣X]]=E[Y]

This one’s a doozy!

Note that when you’re computing E[XY], you’re looking at Sum(xy.fX,Y(x,Y)), ie. the joint PDF or PMF of Random Variables X and Y. If these are independent

We buy some cereal. The box says “16 ounces.” We know that’s not precisely the weight of the cereal in the box, just close. After all, one corn flake more or less would change the weight ever so slightly. Weights of such boxes of cereal vary somewhat, and our uncertainty about the exact weight is expressed by the variance (or standard deviation) of those weights.

Next we get out a bowl that holds 3 ounces of cereal and pour it full. Our pouring skill is not very precise, so the bowl now contains about 3 ounces with some variability (uncertainty).

How much cereal is left in the box? Well, we assume about 13 ounces. But notice that we’re less certain about this remaining weight than we were about the weight before we poured out the bowlful. The variability of the weight in the box has increased even though we subtracted cereal.

Moral: Every time something happens at random, whether it adds to the pile or subtracts from it, uncertainty (read “variance”) increases.

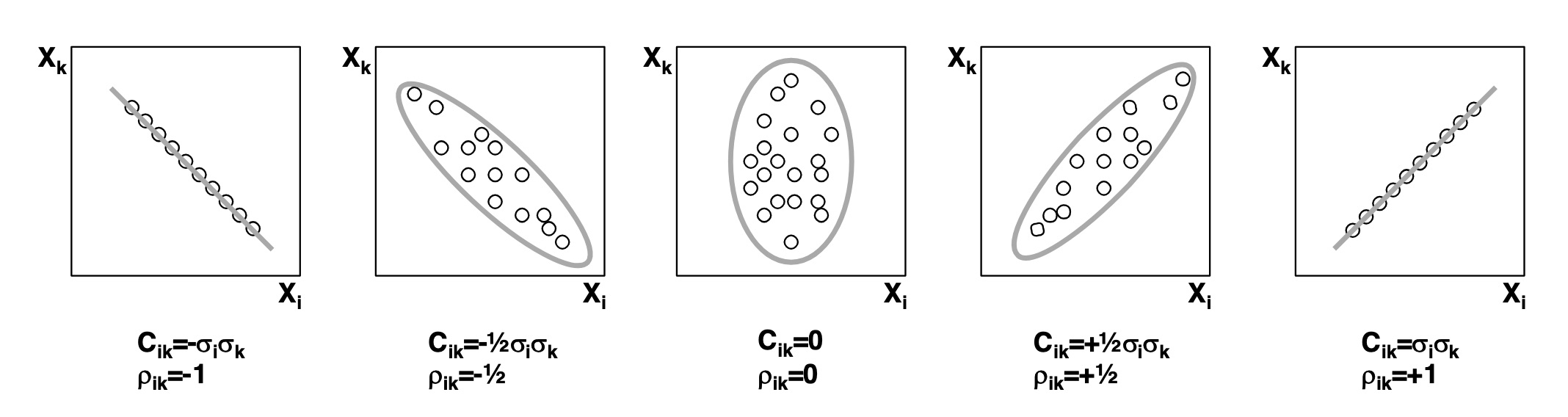

Putting all that stuff up there together. Disjointedness is also called “Mutual Exclusivity”: events have nothing in common in the Sample and Event Spaces. If one happens, the other cannot. In this case, they do not have a joint Probability Distribution at all. So,

E[XY]=0Cov(X,Y)=E[XY]−E[X]E[Y]=−E[X]E[Y]

Now you can look at the PDFs or PMFs of X and Y and expand out that equation2. But what it’s saying with that negative sign is: if X happens, Y cannot.

This means we’re making the result unitless and clamping it to between [0,1]↩

One trick for demonstration purposes is to set the Proability Function to 1A. This means the “Indicator Random Variable” which means X=1 if A happens else zero if A doesn’t. So E[X] just becomes the probability of A. ↩